Savvy tax professionals are familiar with different methods for accelerating tax depreciation, but not all are familiar with cost segregation. “What is Cost Segregation?” is a question that we hear from even the most seasoned tax people. Or they might be familiar with the concept of cost segregation, but don’t understand the details, may have misconceptions or aren’t aware of the full benefits.

Here are the Top 8 Questions about cost segregation that we hear most often and their answers.

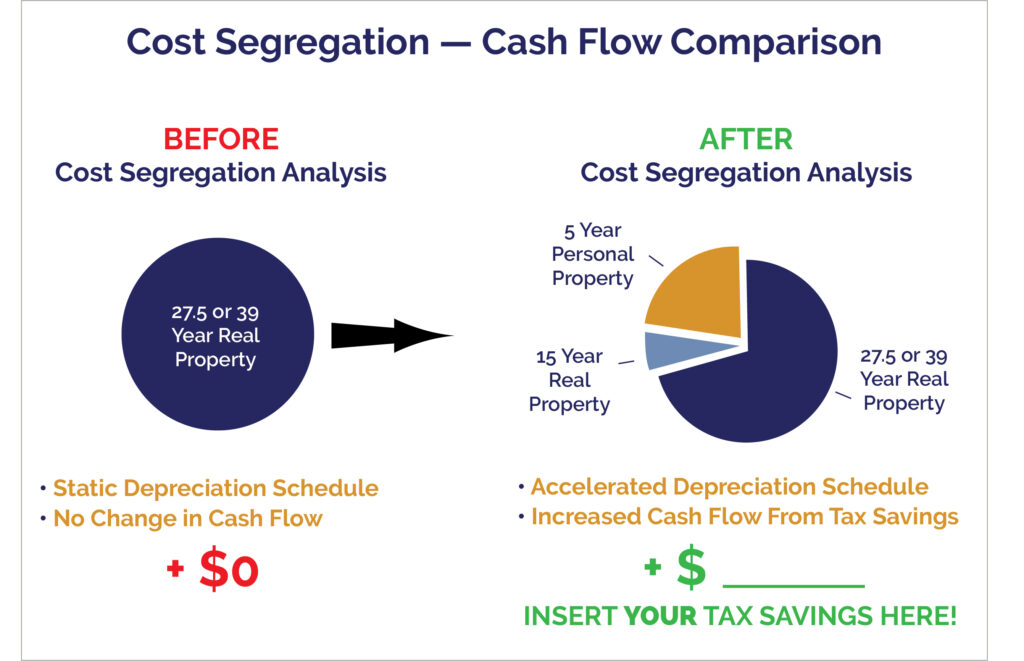

Q1. What is Cost Segregation?

Cost segregation is an often overlooked, valuable tax strategy that can increase return on investment (ROI) and cash flow through accelerated depreciation. It is the process of identifying, and separating personal property assets from real property assets, as shown in the below graphic.

Personal property assets can be written off on a highly accelerated 1-year 100% bonus depreciation, 5-year or 7-year depreciation schedule, instead of the 15-year land improvements or 27.5 or 39-year straight-line depreciation schedule assigned to the physical building structure. This means companies can write-off property much, much faster.

Q2. Why is Cost Segregation important?

When companies and investors build, purchase or remodel commercial property, one of their common concerns is how to minimize costs in order to maximize their ROI. At the end of the day, they want to increase their net cash flow after all expenses and costs have been paid, including Federal and State income taxes. The answer to Question 4 below illustrates the potential accelerated cash flow.

The increased cash flow from cost segregation allows them to reinvest those savings in their business, enabling even greater overall business ROI. It also gives them increased cash flow for paying off debt incurred when financing the project. Sometimes the projected additional cash flow from cost segregation can mean the difference between whether or not they get funding approval for the project.

Unfortunately, real- and personal- property assets are often lumped together on the books, missing valuable write-offs. Correctly classifying or reclassifying certain fixed assets as personal property instead of real property through cost segregation can significantly reduce their depreciable lives and reduce tax liability.

Q3. What types of assets are considered Personal Property?

In an effort to stimulate commercial property investment – purchasing existing, new construction or renovation – the federal government offers certain tax incentives. As stated previously, one of those incentives is allowing building owners to accelerate the depreciation write-offs on the personal property portion.

To get a better handle on cost segregation, it’s important to know which types of assets the IRS Regulations considers to be personal property. These would include any asset that is:

- Not performing a building function, but is inside or attached to the building

- Dedicated to a business process, such as machinery, computers, or furniture

- Easily removable without affecting the building functions

Here are some examples of the types of assets that are considered personal property and often identified and reclassified through a cost segregation study.

- Interior, removable walls

- Custom lighting, fixtures and built-in cabinetry

- Telecommunication and network systems

- Flooring and wall coverings

- Specialty HVAC systems

- Security systems, audio/visual equipment

Q4. Can you show me an example of Cost Segregation savings?

Let’s consider an investor who purchases an existing hotel for $10 million. First of all, to write off the purchase price, the value of the hotel’s assets need to be allocated into different property type and life classes for tax depreciation. This includes the land, land improvements, building, furnishings, decorations, restaurant and bar equipment, fitness center, pool, network wiring and so on.

If the accounting team classifies all these assets as being real property, the total purchase price (less land) is written off at a rate of 1/39th per year for the next 39 years – or $256,410 annually.

However, if 40% of the assets can be re-classified as personal property through cost segregation, they can be written off on the shorter 1-year, 5-year or 7-year schedule, versus 39 years. The below example illustrates the difference in tax savings assuming a 5-year accelerated depreciation schedule (with MACRS half-year convention) and 46.5% combined federal and state tax rate.

The accelerated tax depreciation deductions with cost segregation would generate an additional tax savings cash flow of $1,573,846!

|

|

Before Cost Segregation | After Cost Segregation | |

|

Tax Year |

$10M Real Property Depreciation | $6M Real Property Depreciation |

$4M Personal Property Depreciation |

|

Year 1 |

$256,410 | $153,846 | $800,000 |

|

Year 2 |

$256,410 | $153,846 | $1,280,000 |

| Year 3 | $256,410 | $153,846 |

$768,000 |

|

Year 4 |

$256,410 | $153,846 | $460,800 |

|

Year 5 |

$256,410 | $153,846 |

$460,800 |

| Year 6 | $256,410 | $153,846 |

$230,400 |

| $923,077 |

$4,000,000 |

||

|

6-Year Write-offs |

$1,538,462 | $4,923,077 | |

| Tax Savings | $715,385 |

$2,289,231 |

|

| Additional Tax Savings with Cost Segregation |

$1,573,846 |

||

If 100% Bonus Depreciation were taken, the additional immediate tax savings in Year 1 would be $1,812,308 ($1,931,538 – $119,231)!

In both of these examples, that’s a significant amount of additional cash flow that can be used to reinvest in the business or pay down debt – increasing the highly sought-after ROI.

Q5. Why don’t more business owners use Cost Segregation?

It’s surprising how often we hear the “What is Cost Segregation?” question. Understandably, most business owners or investors aren’t versed in intricate tax laws. That’s typically not their area of expertise. Furthermore, they believe that their accounting firm is well versed in cost segregation, and therefore, are already taking advantage of it. Or they believe that only a very small percentage of real estate assets can be reclassified as being personal property. So why bother since it will be written off eventually?

Unfortunately, unless the company’s accounting firm has highly experienced electrical, mechanical, or architectural engineers on staff, they are likely not qualified to conduct detailed engineering analyses to identify which components qualify, and then use valuation methodology to segregate the related costs for classified assets. Or perhaps they did use cost segregation, but did not reclassify as many assets as they could have, and lost out on potential additional savings. (See Question 7 below.)

From our experience, most of our clients are stunned by how many assets actually are considered personal property for tax purposes. We also like to remind business owners that while they are correct in saying all assets will be eventually depreciated, wouldn’t they rather have the cash today versus waiting 39 years? The time value of money and financial opportunities to reinvest those savings, as illustrated in the above example, speaks volumes.

Q6. How does Cost Segregation work with renovation projects?

For the new construction phase, there is no difference in the segregation process and tax benefits.

The BIG difference is “cash in the trash” that no one writes off against taxable income. All the disposed building components like roofs, chillers, water heaters, drywall, studs, electrical conduit and wiring, light fixtures, etc. have remaining tax basis eligible for write off.

For companies planning a renovation of a recently acquired or existing property, a Fixed Asset Retirement Study can help them find some much-desired cash flow to help fund the renovation. The study identifies the remaining tax net book value of fixed assets before throwing them in the dumpster.

Determination of that basis requires a complex process of retrospective engineering analysis and valuation. In Illinois, every $1 million of write-off creates $465,000 of tax savings or real cash flow! (Potential savings is based on current maximum federal and state tax rates of 37% and 9.5%, respectively. State tax savings will vary in other states, depending on their tax rate.)

Q7. Is there any way to recover overpaid taxes from past projects?

The good news is YES! A little known IRS procedure allows retrospective cost segregation and allocation analyses to determine allowable but unclaimed depreciation, and disposals not written off.

This deduction can be applied to the current year, carried back two years for a refund, or carried forward 20 years against taxable income until used up. Even better news is that amended tax returns are NOT required, just filing a simple form, IRS Form 3115, with the estimated quarterly tax payment or tax return.

Q8. Is there a way that I can estimate MY potential Cost Segregation savings?

Absolutely! Paragon’s easy-to-use Cost Segregation Savings Calculator will show you first-hand how much you could save – whether an acquisition of existing property, new construction, renovation, or leasehold improvements.

Got more questions? Ready to start saving taxes?

While these are the Top 8 “What is Cost Segregation?” questions we often hear, it’s certainly not all of them. Do you have more questions that you would like us to answer? Want to learn more about how cost segregation can increase your business’ cash flow and save money? Contact Paragon today and let’s talk about your particular project.